How to remove inquiries from a credit report

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Fast Credit Repair Solutions editorial disclosure for more information.

Credit scores naturally fluctuate from month to month depending on your usage, payments and transactions. For the most part, your credit score is directly tied to your actions. Occasionally there will be errors on your report that were out of your control, such as with hard inquiries and lines of credit. If you notice a sudden decline in your credit score, even if only by a few points, you may be suffering from the effect of an unwarranted credit inquiry.

Credit inquiries occur when a lender requests your full credit history from one of the credit reporting agencies. These inquiries into your credit history can affect your credit score negatively and will typically stay on your report for up to two years.

Inquiries stay on your record for so long because they reflect how many times you have applied for credit. Lenders use how many times you have applied for credit to judge whether you should be approved for an extension of credit.

In certain circumstances, an unapproved inquiry can be removed from your credit report by sending a credit inquiry removal letter to the credit reporting agency or by disputing it online.

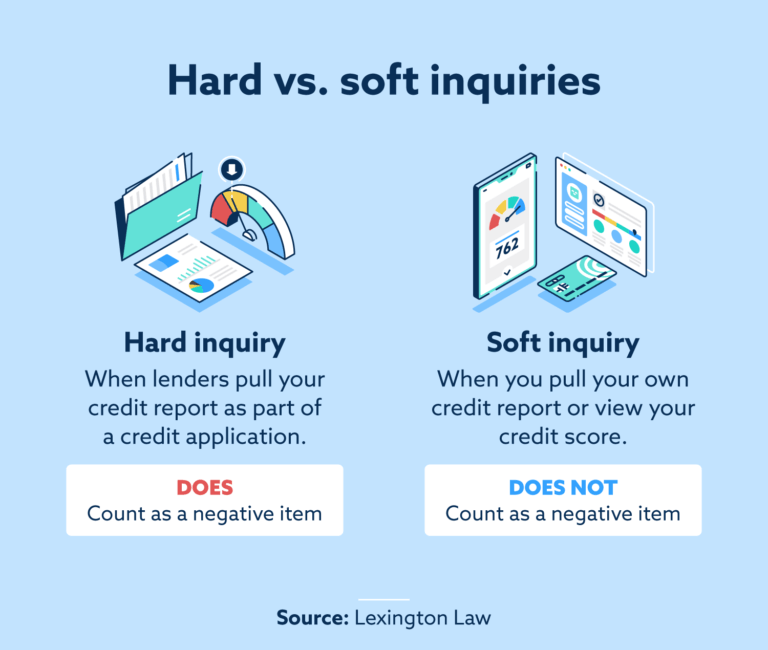

The difference between hard and soft inquiries

Although there is no difference between the data provided in a hard and soft inquiry, they do not affect your credit the same way. A common misconception is that checking your own credit history will negatively affect your score, but this is not true. When you check your own credit history, it is considered a soft inquiry and will not show on your credit report or affect your score.

Hard inquiries, by contrast, occur when a lender pulls your credit report. A lender may pull your credit history while going through an application for a new loan, a new credit card or any line of credit. Additionally, banks and property managers may pull your credit while setting up accounts or determining approval for an apartment.

Occasionally, a hard credit report can sometimes be pulled without your knowledge, approval or without your full understanding. Hard inquiries that were pulled without your request can be removed from your credit report under the Fair Credit Reporting Act.

How do credit inquiries affect your credit score?

Hard inquiries count as minor negative entries and account for 10 percent of your credit score. Although the exact effect on your credit score will vary depending on your credit history and current standing, you can typically expect to see a one to five point drop in your overall credit score.

Although the exact hit to your credit score will vary, you can expect to see drops in your score when these inquiries start to add up. Occasionally lenders will either pull your credit by mistake, pull your credit multiple times or pull your credit without your knowledge whatsoever.

Can you remove inquiries from your credit report?

Hard inquiries can be removed from your credit history if they occurred without your approval. If you did not have knowledge of the hard inquiries pulled from your credit profile, you have the right to ask for the inquiry to be removed.

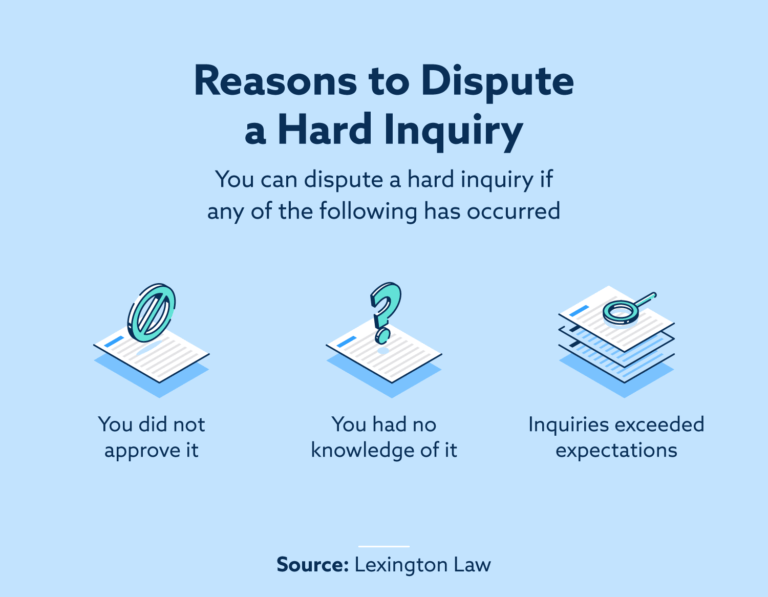

You can remove a hard inquiry if:

- The inquiry occurred without your knowledge.

- The inquiry occurred without your approval.

- The number of inquiries exceeded what you expected.

How to send a credit inquiry removal letter

To send a credit inquiry removal letter, you should contact any credit reporting agency that is reporting the inquiry. Credit inquiry removal letters can be sent to both the credit reporting agencies and the lender who issued the credit inquiry.

1. Send the credit inquiry removal letter via certified mail

Certified mail is a way in which the sending and receiving of a letter or package is recorded. This form of mail will give you proof that the credit issuer or lender received the proper first notification to remove the hard inquiry.

2. Notify the lender first

Notifying the lender before you send a removal notice is necessary if you plan to take the dispute further to court. This is the proper first step for removing hard inquiries.

3. Include a copy of your credit report

Including a copy of your credit report with the highlighted unapproved hard inquiries may help with referencing your case. Although the credit reporting agencies will have easy access to your report, a hard copy will help investigators when processing your request.

4. Send to the appropriate credit bureau

It is important to send your letter to the credit bureau with a record of the hard inquiry you want removed. Below are the addresses for each bureau:

Equifax

P.O. Box 740256

Atlanta, GA 30374-0256

Equifax Dispute Information Center

Experian

P.O. Box 4500

Allen, TX 75013

Experian Dispute Information Center

TransUnion LLC

Consumer Dispute Center

P.O. Box 2000

Chester, PA 19016

TransUnion Disputes Information Center

Credit inquiry removal letter template

Date

Your name

Your street number, street name

City, state, zip code

Your phone number

Social Security Number

Name of credit bureau

Re: Reporting Unauthorized Credit Inquiry

To whom this may concern,

I am writing to request the removal of unauthorized credit inquiry/inquiries on my (name of the credit bureau—Equifax, Experian and/or TransUnion) credit report. My latest credit report shows (number of hard inquiries you are disputing) credit inquiry/inquiries that I did not authorize.

I am writing to dispute the following inquiries and ask for their removal from my credit report.

| Item No. | Creditor | Account |

|---|

Please have these/this unapproved inquiries/inquiry removed from my credit report within 30 days, as it is harming my ability to obtain new credit. I would appreciate a copy of my credit report once this issue is resolved.

Thank you for your assistance.

Sincerely,

(Your Name)

How to stay on top of negative credit report entries

Removing questionable negative items from your credit profile can be a long and time-consuming process that can seem daunting. Although a few points’ difference may not seem like a large priority, it is important to stay on top of these entries before they add up and get out of control.

If keeping your credit score high or improving your credit score is a top priority, Fast Credit Repair Solutions may be a good option for you. Fast credit repair services can help you with addressing questionable negative items on your credit report as you work on improving your credit.

Cynthia Thaxton has been with Fast Credit Repair Solutions since 2014. She attended The College of William and Mary in Williamsburg, Virginia where she graduated summa cum laude with a degree in International Relations and a minor in Arabic. Cynthia then attended law school at George Mason University School of Law, where she served as Senior Articles Editor of the George Mason Law Review and graduated cum laude. Cynthia is licensed to practice law in Utah and North Carolina.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.

When working with a credit lawyer, you should carefully read their contract to understand how much you’re paying and what services they’ll execute for you. You should also walk away if they demand payment upfront. According to the FTC, they’re not allowed to ask for payment before services are executed.

Using Nonprofit Organizations

You can seek help from nonprofit organizations if you’re unable to afford a credit lawyer. Many nonprofits offer services like credit counseling, budgeting workshops and other financial resources. They may also have volunteer lawyers available to help as well.

Nonprofits are sometimes limited based on their budget and availability of staff and volunteers, so you should ask about their process if you’re interested in taking this route.

Even if you’re planning to work with a nonprofit, you should still look at their reviews and do some research to ensure you’re working with a legitimate organization.

How Can I Avoid Scams?

You can avoid scams with credit lawyers by doing your research, knowing what questions to ask and becoming familiar with your legal rights.

Just like any service, you should check out the lawyer’s reviews and testimonials to see what you can expect when working with them. You can also check their records with their state bar association. Here are a few sites to research potential credit lawyers:

- Better Business Bureau

- American Bar Association

- State Bar Association

Next, you should come prepared with a list of questions and a mental note of warning signs when first consulting with each lawyer. Some questions include:

- What experience do you have working on credit-related cases with people in my situation?

- What services will you execute for me based on my situation?

- What will this cost me?

You should also watch for the following red flags:

- Asks you to pay upfront

- Encourages you to misrepresent your information

- Offers to sell you a social security number

- Doesn’t explain your legal rights, like that you’re able to repair your credit yourself

- Promises to deliver results in a specific time frame or at a specific point increase

- Claims they can remove correct information from your credit report

Finally, you should get familiar with the basics of some of the laws we mentioned earlier in the post. That way, you can quickly determine if the lawyer has the right experience and is knowledgeable enough to help you.

Do I Need a Lawyer to Fix My Credit Score?

No, you don’t need a lawyer to fix your credit score. You can do anything a credit lawyer can do, but your best option depends on a variety of things.

Credit lawyers likely have experience in many areas you may not have the time to learn. These include:

- Reviewing credit reports and dealing with credit bureaus and creditors

- Understanding credit laws and consumer rights

- Dedicating time throughout the day to call and send letters to creditors and the bureaus

Unless you can dedicate the time needed to learn and diligently work through everything, you might put yourself at risk of missing crucial details or otherwise making a costly mistake. For example, a credit bureau can deny your dispute if you don’t provide the correct or enough documentation.

This can cost you time, money and points on your score if you’re unable to resolve it. However, the best choice for you depends on your personal preferences, how much time and money you’re able to dedicate, and the complexity of your situation.

Do I Need a Lawyer for Debt Settlement?

No, you do not need a lawyer for debt settlement. However, you may want to consider using a lawyer for the same reasons we mentioned above.

Working with a lawyer can give you the peace of mind that someone with the right experience and knowledge is on your side.

Fast Credit Repair Solutions works with a network of lawyers who have years of experience working on credit-related cases. Give us a call today to learn more about our credit repair services and how our team of lawyers and paralegals can help you make informed decisions about repairing your credit.