The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Fast Credit Repair Solution editorial disclosure for more information.

Even if you didn’t purchase a home in America last year, you likely heard chatter about the record-breaking housing market that has continued to be a competitive landscape for buyers.

While time will tell the lasting impacts of the COVID-19 pandemic on the housing market, by comparing pre- and mid-pandemic data, we begin to see that there are a few key insights into how the pandemic has impacted the market.

We know that the current housing market is a seller’s market due to low mortgage rates driving demand, which has driven prices up. The low inventory of homes was a factor before the pandemic started, but the rising cost of lumber has led to a decrease in newly constructed homes and the pandemic itself has encouraged many sellers to hold off listing their homes until the virus is minimized.

The current house-buying market is also competitive and fast-moving. In 2020, buyers searched for an average of eight weeks and looked at a median of nine homes, according to the National Association of Realtors.

We’ll dive into the statistics and factors affecting the current housing market below. You can also skip straight to the infographic for even more key insights.

How COVID-19 has impacted the housing market

The pandemic has compounded existing difficulties and added new factors into the home-buying process. Let’s examine a few of the main driving forces behind the current housing market below.

Where people are moving

One of the interesting factors associated with the housing market amid the COVID-19 pandemic is where people are choosing to live. According to the 2020 National Movers study by the moving company United Van Lines, Idaho experienced the most inbound moves and New Jersey experienced the most outbound.

The report also found that New York, New Jersey, Connecticut and Maryland make up four of the top 10 states with the most outbound moves. When it came to inbound moves, the southern and western states of Idaho, South Carolina, Oregon, South Dakota and Arizona ranked in the top five with 250 or more moves.

While some are choosing to move to the suburbs, the American urban centers continue to be attractive places to live, as evidenced by a Zillow report that found home value growth, sales volume and Zillow web traffic in urban areas has kept pace with or exceeded levels in suburban areas.

What people are looking for in a home

Our homes became incredibly important in 2020. Not only were they where we cooked and slept, but we also began working from home as the COVID-19 pandemic shut down offices across the country. As the amount of time spent at home increased, several aspects of houses have become more attractive to homebuyers during the pandemic.

According to , for-sale listings on the site mentioning a home office description jumped 10 percent, indicating a growing need for private spaces in the homes of remote workers. Zillow also found that more Americans are valuing kitchens and large outdoor spaces more due to social distancing recommendations.

Increasing home prices

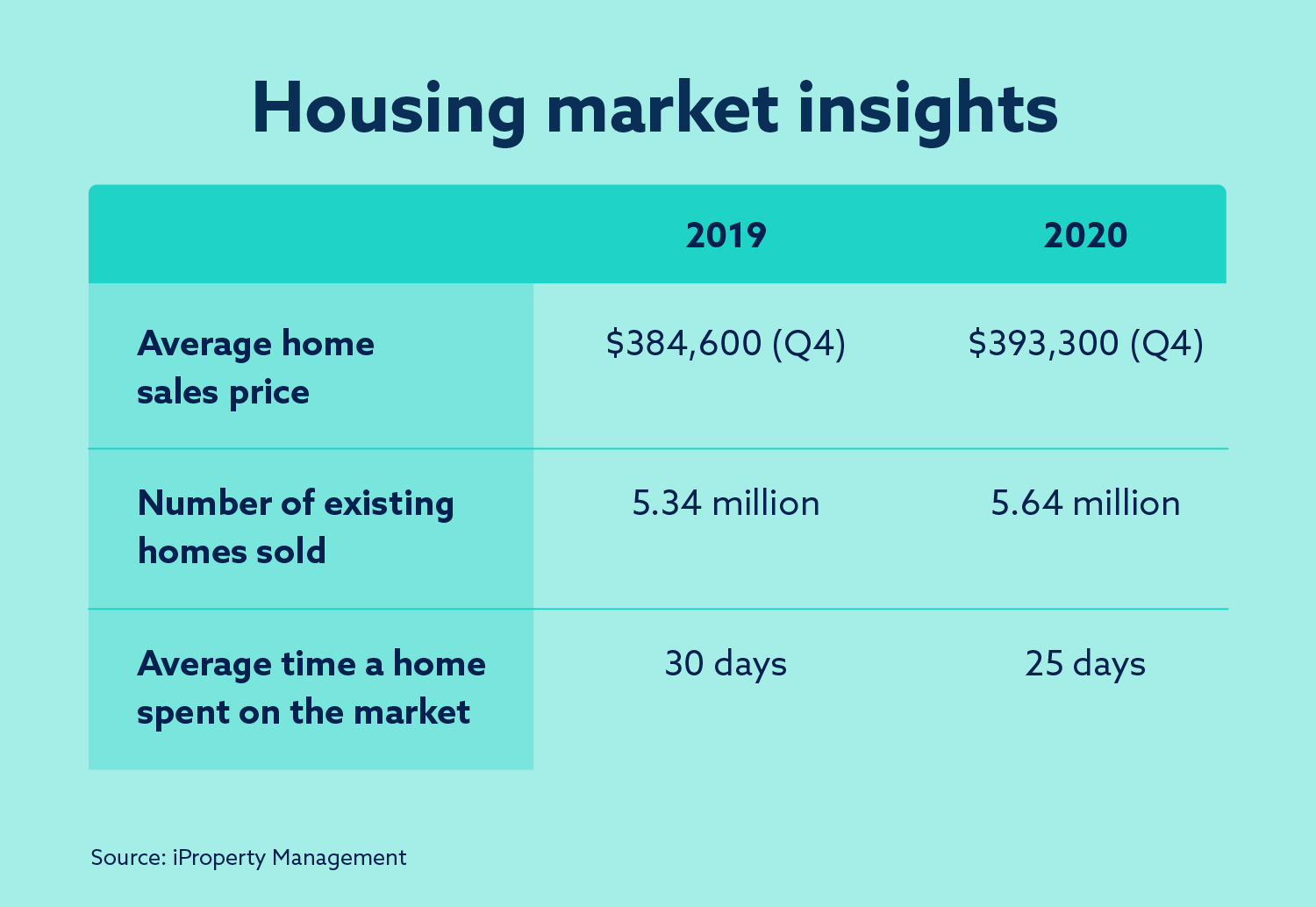

While the early months of the pandemic dropped the sales of existing homes nearly 18 percent from March to April 2020, June sales surged by 21 percent. As the number of homes sold began to rise, so did U.S. home prices. The S&P CoreLogic Case-Shiller 20-city home price index found home prices climbed 10.1 percent in December from a year earlier, which is the largest jump since April 2014.

One of the driving factors behind the growing home prices is the low inventory of homes on the market. While this was also true of the housing market in the pre-pandemic days, there were less than two-thirds of the number of homes on the market in August 2020 as there were a year before, according to the Federal Reserve Bank of St. Louis. As the demand for homes grew during the pandemic, buyer bids increased on the number of available homes on the market in order to purchase a home.

Another factor that’s further diminishing the number of homes available for purchase is the rising cost of building a home. According to the National Association of Homebuilders, the increase in lumber prices in 2020 caused the price of an average new single-family home to increase by $16,148, and the market value of an average new multifamily home to increase by $6,107. As the cost to build increases, builders are slowing production, exacerbating the housing shortage.

Comparison of the housing market before and during the pandemic

There are some notable differences between the pre- and mid-pandemic housing markets, including how home sale prices have risen and how the average time on the market has decreased, indicating a competitive market. Take a look at how the housing market has changed over the course of the COVID-19 pandemic below.

Average home sales prices

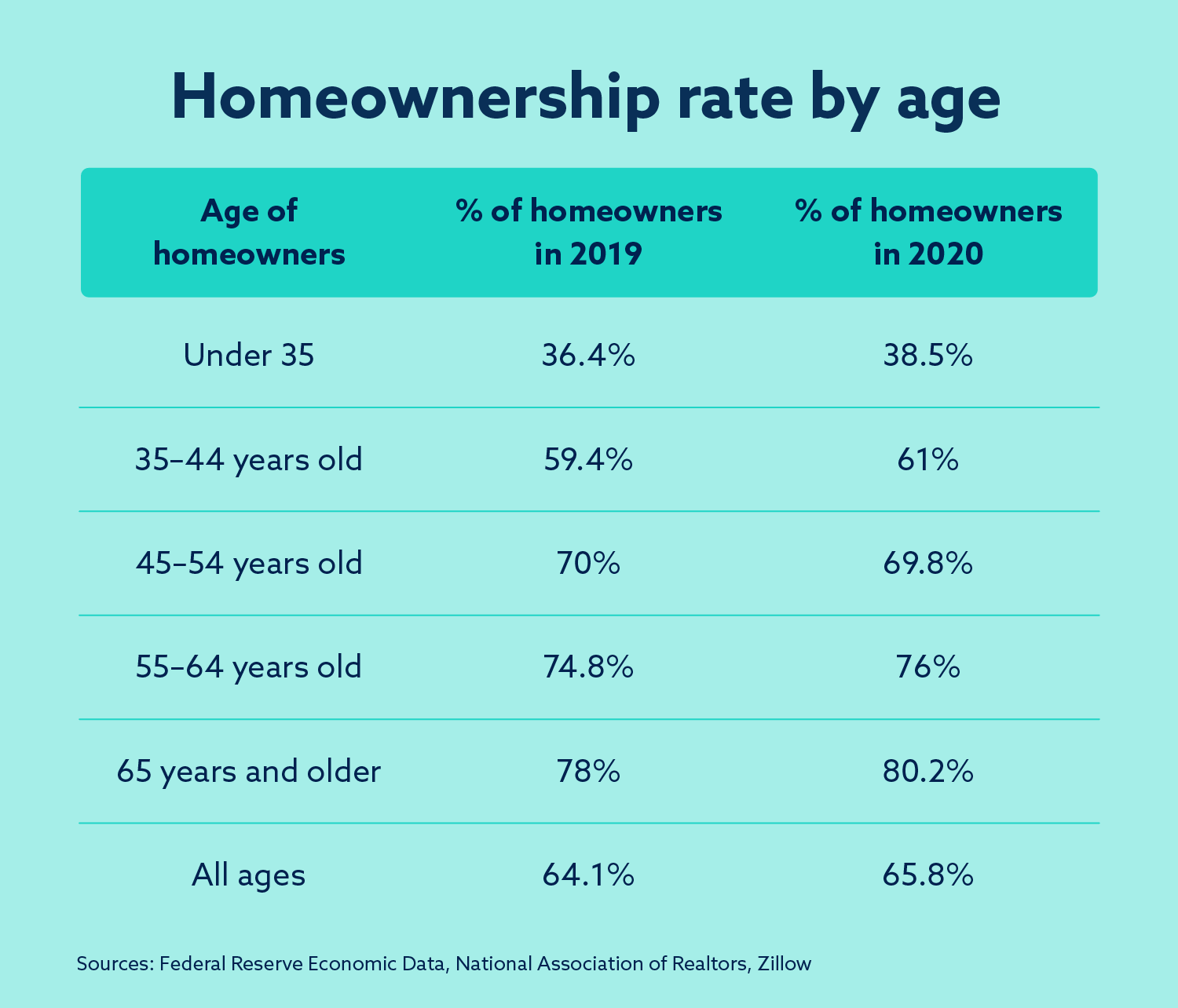

Homeownership rate by age

Current advantages of buying a home

While this is a seller’s market, there are still attractive advantages to buying a home during the pandemic if you can. One big advantage right now is that mortgage interest rates are at record lows, resulting in lower monthly mortgage payments. And while you might not feel comfortable touring a home in person during the pandemic, the number of 3D home tours during the COVID-19 pandemic has risen, which means that you can still have a quality home tour without leaving your home. This is an added benefit if you’re looking to move to a new city or state.

Current disadvantages of buying a home

Buying a home during the pandemic isn’t a good move for everyone. You may be better off waiting to buy depending on your financial situation. The number of available homes is lower than it has been historically. This is due to the demand for homes growing and because sellers are waiting until the pandemic is over to list their homes for fear of not being able to find a new home to buy. With fewer houses available, you may need to sacrifice some of your must-haves to find a home in your price range or desired area.

Another slight disadvantage to purchasing at this time is that buyers may have a harder time moving as friends and family are following pandemic guidelines and avoiding close contact with those outside of their immediate household.

Factors to consider as you determine your readiness to buy a home

If you’re considering buying a home in 2021, there are a few questions you should consider before diving into your search.

Job security

The pandemic has brought with it a feeling of uncertainty for many regarding their employment, but job stability is an important factor in determining your readiness to buy a home. Before you make a 30-year commitment to a mortgage, it’s important you feel safe in your employment situation or that you have enough saved so that you’d feel comfortable with your mortgage even if your employment felt precarious.

Down payment

A down payment on a home is a big commitment. Even with the current low mortgage rates, there are hidden costs associated with a new home including closing costs, taxes and money for repairs, as well as furniture and other home items. If you can afford a down payment and have some funds left over for the inevitable costs that come with homeownership, you’ll be better prepared to own a home.

Your credit score

Your credit score is a huge factor when it comes to determining the kind of loan you might qualify for and the interest rate you’ll pay on a mortgage. In 2021, the minimum credit score needed to purchase a home could be anywhere from 500 to 640 depending on the type of mortgage you want. If you have a low credit score, lenders may saddle you with a high down payment or a high interest rate.

While there are many factors to consider as you start gauging your readiness to purchase a home in 2021, it’s important to remember that homeownership is a huge step, and you’ll be happy you have your financial house in order before you make that leap. Once you begin to lay the groundwork for purchasing a home, you’ll start to feel more confident in the process and your ability to own a home.

Infographic